.jpg)

Privatising public sector companies would have encountered significant opposition from their managers as well as from strong unions.

One may fault this government for incompetence, corruption, and delayed action but it cannot be faulted for lacking a vision.

The drug Glivec was a genuinely new and important discovery deserving of patent protection.

The Budget is disappointing because it refuses to fundamentally repudiate fiscal populism.

The country's growth cannot be sustained without a revitalised state that performs more limited functions, but performs them well.

Active participation in multilateral co-operation can be India's response to China's growing economic presence.

The grouping has influenced China, but Germany will be more difficult.

Greece was an opportunity for the IMF to set a precedent for an orderly debt resolution programme.

The dispersion of global economic power augurs well for the role of ideas in policy-making.

There is a need for coordination among emerging economies on managing capital flows and exchange rates, and China's exchange rate policy can help. That it is ready to be more flexible is welcome

He should not publicly press India to open its financial sector.

Indirect tax reforms may help strengthen the Indian state and hence long-run growth.

India should push the World Bank to focus on generating ideas and technology.

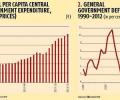

If India reverts to a trend growth of say 8-plus per cent soon, the time is ripe for commencing the process of fiscal consolidation, especially since her public sector balance sheet remains so fragile, says Arvind Subramanian.

China shows that strong public finances are important for global leadership.

The current Euro-Atlantic Monetary Fund must become an International Monetary Fund.

The RBI's big decision is not how much to ease but whether to monetise the fiscal deficit.

Residents did not bolt for the exit, dampening the crisis' financial impact.

We must use the crisis to find the sensible middle ground between finance fetishism on the one hand, and status quo statism on the other.

The risk of worldwide protectionism looms, especially if the dollar appreciates.